2016 Jun–Jul

Boston in the Media: The Exception Became the Rule

After the referendum result, Boston became the most-cited symbol of the Leave vote

in national media coverage. BBC News, Sky News, and Channel 4 all ran features in

the town in the days after the result. Interviews with Boston Leave voters were

broadcast nationally and interpreted as representative of why Britain voted Leave.

The problem: Boston was the exception, not the rule. Its combination of

high EU immigration and high Leave vote was unique precisely because its EU

immigration was so visible. The majority of high-Leave areas had very little

EU immigration. The immigration narrative — compelling and vivid in Boston —

was being generalised to explain a phenomenon that, everywhere else, had almost

nothing to do with immigration.

This media amplification locked in the incorrect causal narrative: "people voted

Leave because of immigration." It crowded out the more accurate and more troubling

story: "people voted Leave because a decade of austerity had left them with a

legitimate grievance, and the campaign gave them immigration as the explanation."

The distinction matters enormously for policy. The "immigration caused Brexit"

narrative implies that restricting immigration would have prevented it or would

satisfy the underlying grievances. The "austerity caused Brexit" narrative implies

that the underlying grievances remain intact — and have since been compounded by

Brexit's own economic costs.

But even the word "austerity" can mislead, if it conjures only Treasury spreadsheets

and GDP charts. The actual experience of the grievance was granular and daily.

Middle England cities and towns were asking — not rhetorically, but in the ordinary

course of life — why their local bus route had been cancelled. Why the swimming

pool had been sold off, rebranded, and now cost twice as much to enter. Why the

planning portal crashed every time you submitted an application. Why it took

forty-five minutes on hold to speak to the council about a missed bin collection.

Why Transport for London — with its Oyster card, its real-time apps, its

frequent and comprehensible network — felt like a piece of infrastructure

from a different country, available only to the people who happened to

live where the money was.

This was not abstract. These were the touchpoints through which the state made

itself legible — or stopped doing so. The decade after 2010 was the decade in

which local government quietly stopped being something people encountered as a

functioning service and became something they encountered as an absence: a closed

library, a defunded youth centre, a website that told you to call a number that

put you on hold. The grievance that Brexit crystallised was partly about trade

exposure and public spending aggregates, but it was also about this: the daily

experience of a state that had retreated, and left nothing in its place.

The relevant Brexit voter is not only the agricultural worker in Boston competing

with EU labour. It is also the resident of a medium-sized English town watching

the leisure centre close, the bus timetable shrink, and the council website fail

— and being told, by a campaign with a red bus and a large number, that the

explanation and the remedy were both the same thing: leaving the European Union.

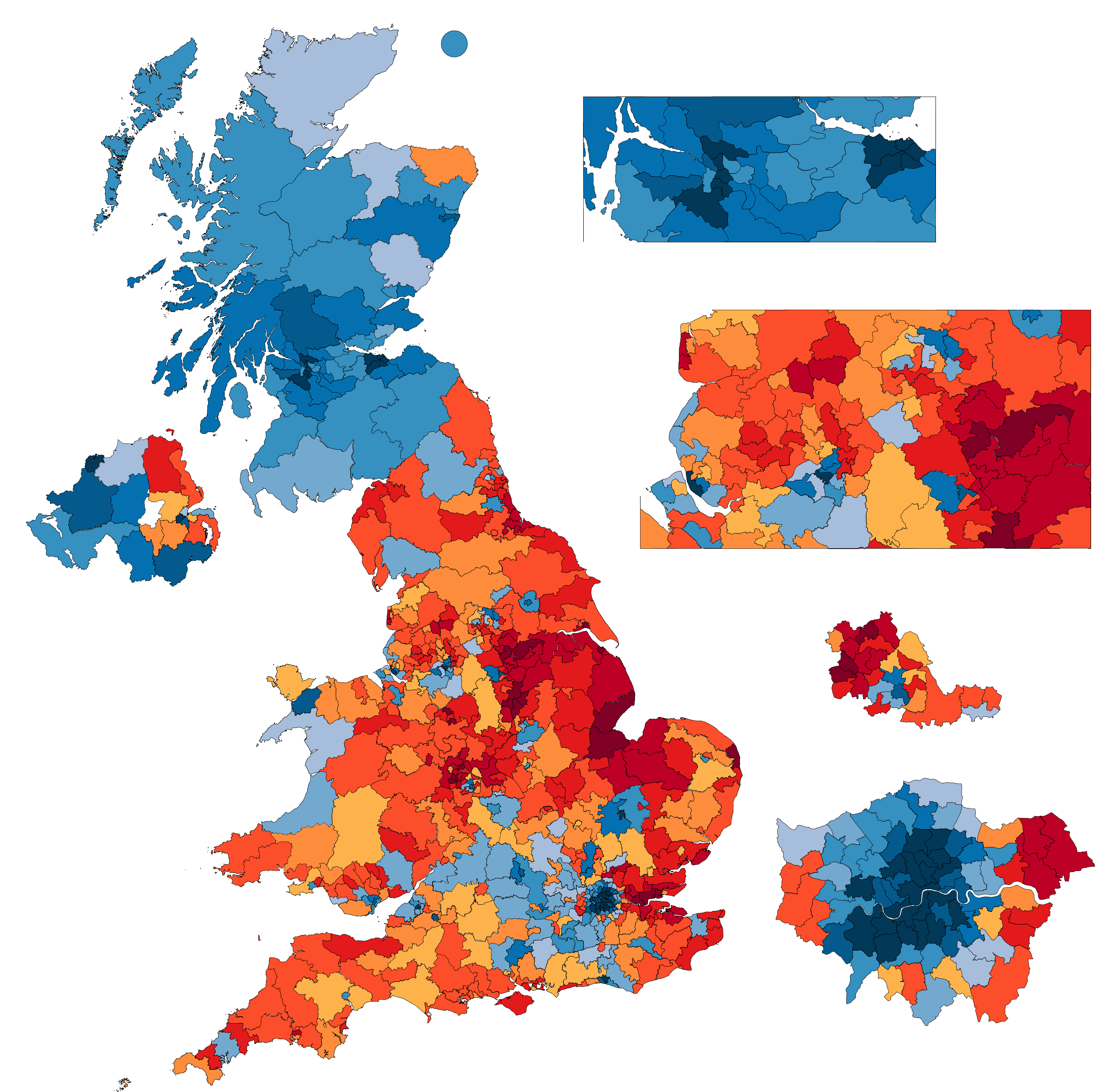

The Leave Vote in Rural and Small-Town England

Boston's story — high immigration, high austerity, highest Leave vote — became the face of Brexit in national media. But most Vote Leave communities looked like this: small towns with visible decline and very little EU immigration.

Vote Leave sign in Belper, Derbyshire. Belper is in an area with average EU immigration but high austerity exposure — more representative than Boston of the typical Leave community.

Wikimedia Commons

"Will Brexit ever mean Brexit?" — a question painted on a coastal wall in Northumberland, a region with high austerity and low EU immigration

Wikimedia Commons